Newsletter Mercados

July 17, 2026 • 1133 words • 0 sources

Listen to this newsletter as a podcast

Three voices, natural conversation. Listen while you catch up.

Global Context

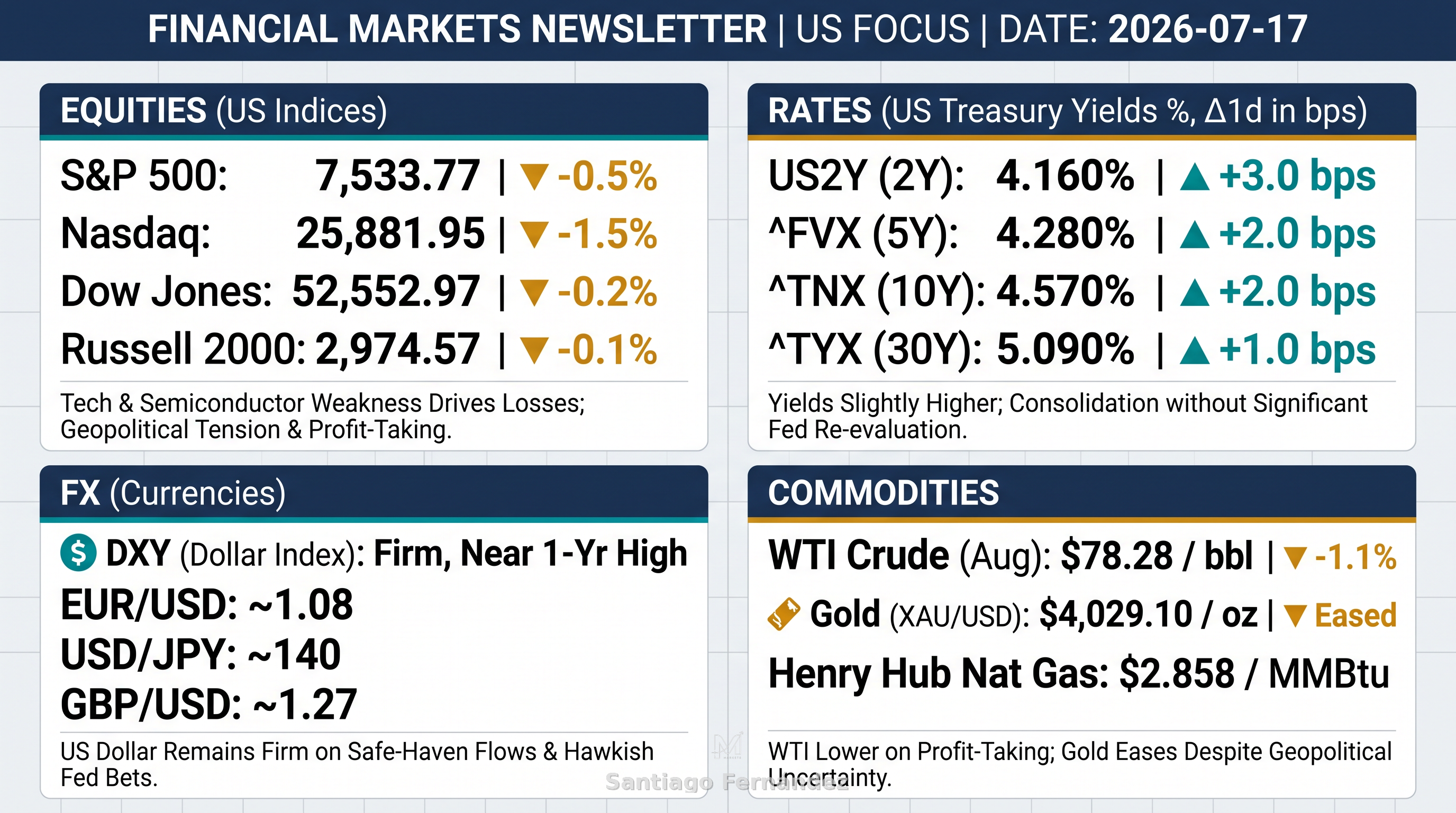

Thursday's session on Wall Street closed mixed, with the S&P 500 down 0.5% to 7,533.77, the Dow Jones down 0.2% to 52,552.97, the Nasdaq Composite down 1.5% to 25,881.95, and the Russell 2000 down 0.1% to 2,974.57. Losses were led by the technology and semiconductor sectors amid profit-taking following mixed corporate earnings. In Europe, the FTSE 100 rose 0.5% to 10,572.2, while the DAX fell 0.34% to 24,915 and the CAC 40 fell 0.58%. In Asia, the overnight session showed caution, with pressure on technology stocks. Geopolitical tensions between the U.S. and Iran continue to be the focus of attention, raising oil volatility and generating safe-haven flows into the dollar.

Interest Rates

US Treasury yields closed slightly higher on Thursday: the 2-year rose 2.9 bps to 4.155%, the 5-year +2 bps to 4.28%, the 10-year +2.2 bps to 4.568%, and the 30-year +1.4 bps to 5.097%. The 2s10s curve stood at 41.3 bps and the 5s30s at 81.7 bps. The move is interpreted as consolidation at current levels, without a significant re-evaluation of Fed expectations. Hawkish comments from Governor Cook, warning of potential hikes if inflation does not subside, did not materially alter pricing. In today's pre-market, Treasury futures remain stable, with the 10-year around 4.57%.

Sovereign Debt

The U.S. corporate debt market showed resilience on Thursday, though movements appear to be driven by market beta rather than active flows. No specific data was reported for credit spreads or ETF flows (HYG, LQD, JNK). Financing conditions remain stable, with no signs of stress. Geopolitical caution could favor relative demand for higher-quality assets, but conviction remains limited.

Corporate Credit

Corporate credit remains stable, with spreads largely unchanged. No significant active flows were observed in HYG or LQD. The market appears to be in wait-and-see mode, awaiting new macro or geopolitical catalysts. The lack of stress in funding conditions suggests that risk appetite has not sharply deteriorated, but caution prevails.

Foreign Exchange

The US dollar remains firm, backed by safe-haven flows amid geopolitical tensions and bets on a hawkish Fed stance. The DXY showed no clear directional movement at Thursday's close but remains near its highest levels in over a year. EUR/USD trades around 1.08, USD/JPY near 140, and GBP/USD at 1.27. Attention is on Fed comments and developments in the Middle East.

Commodities

WTI crude for August closed lower on Thursday, at $78.28 per barrel (-1.1%), pressured by profit-taking despite geopolitical tensions. Henry Hub natural gas fell to $2.858 per MMBtu. Gold (XAU/USD) eased to $4,029.10 per ounce, from $4,048.39. In today's pre-market, WTI is trading around $78.50, with volatility driven by developments in the Strait of Hormuz. Gold could find support if geopolitical uncertainty intensifies.

Equities

On Thursday, the S&P 500 fell 0.5% to 7,533.77, the Nasdaq 1.5% to 25,881.95, the Dow 0.2% to 52,552.97, and the Russell 2000 0.1% to 2,974.57. Weakness in semiconductors and AI companies drove losses, despite strong quarterly results from Morgan Stanley, BlackRock, and PNC Financial. Sentiment was impacted by profit-taking and geopolitical tensions. Today's futures point to a mixed open: ES near flat, NQ slightly negative, YM stable. Focus is on technical levels and any escalation in the Middle East that could affect risk appetite.

Cryptocurrencies

Bitcoin (BTC/USD) and Ethereum (ETH/USD) corrected slightly in the last 24 hours. Bitcoin trades around $63,910, with a 1.36% drop, while Ethereum stands at $1,845, -2.45%. In today's pre-market, BTC trades near $62,953 and ETH at $1,849. Lack of bullish momentum and institutional profit-taking limit the movement. Key levels to watch are $62,000 for Bitcoin and $1,800 for Ethereum.

Conclusion

Markets face a cautious session, with mixed futures and attention focused on geopolitical tensions in the Middle East. The lack of macroeconomic catalysts leaves investors focused on safe-haven flows and technical positioning ahead of the weekend. Treasury yields remain stable, while the dollar benefits from risk aversion. Oil and gold could experience additional volatility. Directional conviction remains limited, and risks are skewed towards unexpected geopolitical events.